CRDO: Solving the Connectivity Bottleneck— Why the Post-Earnings Dip Is the Entry You've Been Waiting For

FY2026 revenue tripled. Net income rose 5×. The stock dropped 12%. Here's what the market got wrong.

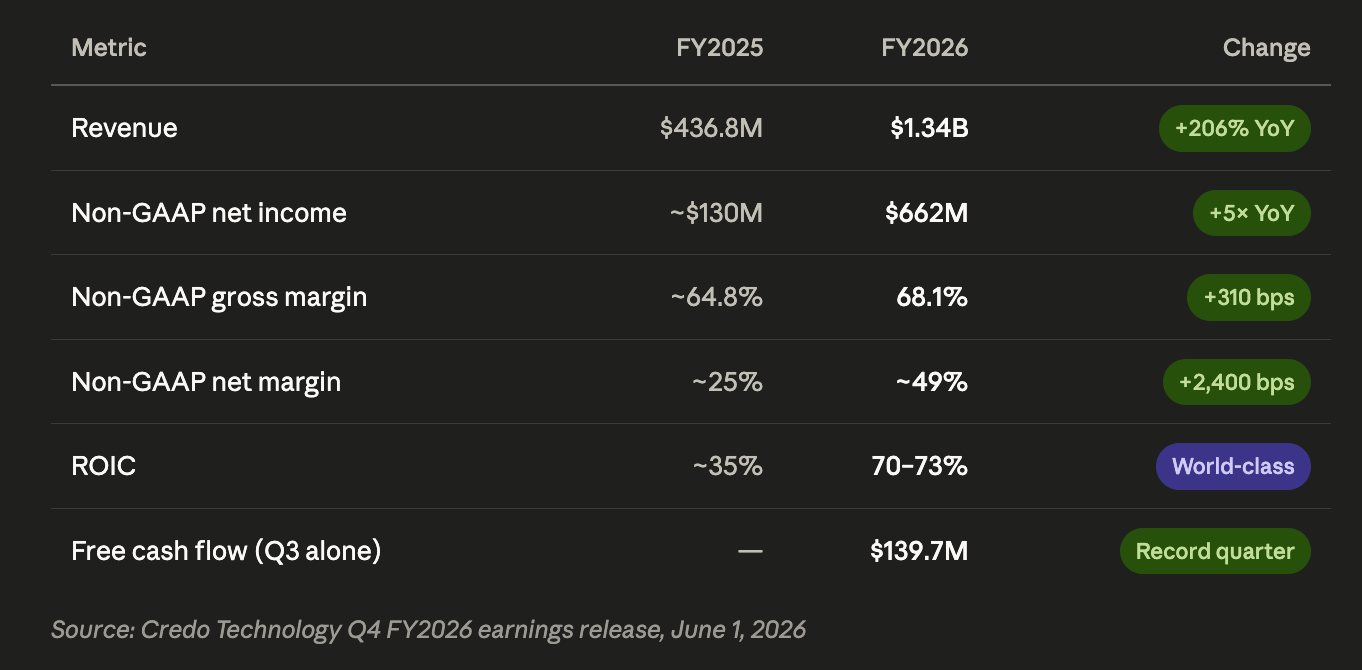

"Fiscal '26 marked another defining year for Credo. Revenue exceeded $1.3 billion, more than tripling year-over-year, while non-GAAP net income increased more than 5x to $662 million."

- Bill Brennan, President, CEO & Chairman, Credo Technology

After years watching semiconductors cycle through booms, busts, and everything in between — from the dot-com era to the mobile revolution to the cloud buildout — I can say without hesitation: what Credo Technology Group (NASDAQ: CRDO) is doing right now is among the most extraordinary financial performances I have ever seen from a hardware company. Revenue tripling in a single year. Net income is rising more than 5x. Gross margins above 68%. A ROIC of 70%+. These are software company metrics coming out of a semiconductor business.

And then the stock dropped 12% after-hours on June 1st.

That is your opportunity. Let me explain exactly why.

The Business

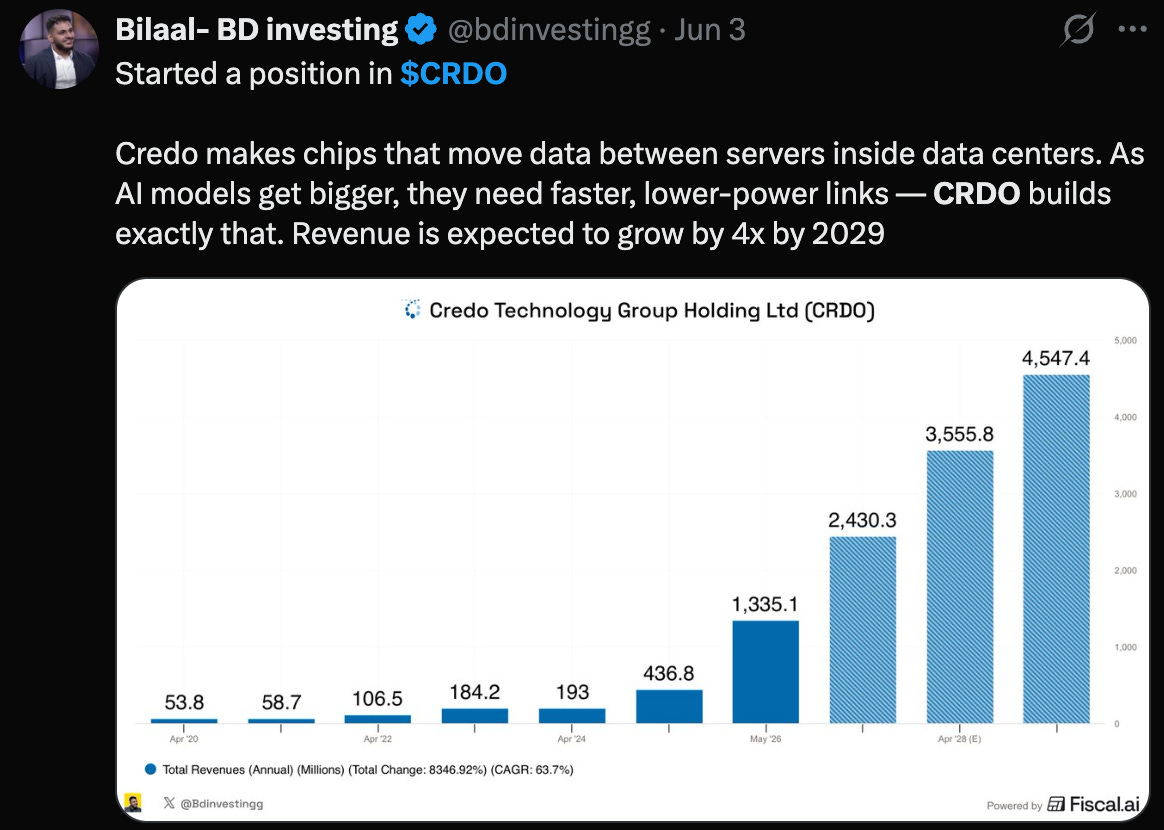

Credo makes the semiconductor chips embedded inside the purple cables connecting NVIDIA GPUs inside Amazon, Microsoft, Meta, and xAI’s AI data centers. These are called Active Electrical Cables (AECs) — copper cables with a smart signal-processing chip at each end that amplifies, cleans, and re-times the signal.

Think of a regular copper cable as a garden hose. Data leaks, weakens, and degrades over distance. Credo’s AEC is a smart pump system — it takes that degraded signal and restores it to perfection, allowing data to travel faster and farther with zero leakage.

Inside an AI training cluster housing thousands of NVIDIA H100 or GB200 GPUs, every chip needs to communicate with every other chip at blinding speed. AECs connect the GPUs to each other and to the network switches. The denser the cluster, the more AECs you need. And GPU clusters are getting denser every quarter.

AWS CEO Matt Garman didn’t need a press release to confirm this. He posted a photo of Trainium AI chip racks showing Credo’s purple cables right there in the rack. That image is worth a thousand earnings calls.

This is Credo’s core business. And it is exploding.

FY2026: A Year That Rewrites the Semiconductor Playbook

Let the numbers speak:

The quarterly progression tells an even more dramatic story:

Q1 FY2026: $223.1M (+274% YoY)

Q2 FY2026: $268M (+272% YoY)

Q3 FY2026: $407M (+200% YoY, +52% sequential — a blowout)

Q4 FY2026: $437M (+157% YoY) ✅ Beat $433.3M consensus

Q4 non-GAAP EPS came in at $1.16 versus $1.03 consensus — a 12.6% beat. Non-GAAP gross margin hit 68.3%, above the guided 64–66% range. Non-GAAP net income for Q4 alone was $226.7 million.

Credo generated more profit in a single quarter than its entire revenue three years ago.

Why the Stock Fell 12% After-Hours (And Why That’s Irrational)

The market was pricing in a Q1 FY2027 revenue guidance raise to $500M+. Management guided $465–475M (midpoint $470M) — exactly in line with analyst consensus of $470.4M. The stock dropped 12% for being... exactly right.

This is the “priced for perfection” tax on high-growth stocks. It is not a business deterioration. It is not a thesis crack. It is a classic post-earnings expectations reset on a beta-3.18 stock where investors had been bidding up the pre-earnings anticipation.

Let’s be clear about what Q1 FY2027 guidance of $465–475M actually means:

+50%+ year-over-year growth in the next quarter alone

Sequential growth from Q4’s $437M

Gross margin guided 67–69% — maintaining premium margins

That is an exceptional result by any measure outside of the hyper-elevated expectations Credo itself has trained the market to expect. The stock fell not because anything went wrong, but because “extraordinary” wasn’t “extraordinary enough” for a single quarter of positioning.

For long-term investors, this distinction is everything.

The FY2027 Roadmap: From $1.34B to $2.4B+

Management’s FY2027 guidance is more than 80% revenue growth — implying $2.4B+ in revenue for the fiscal year ending April/May 2027. The key driver powering this acceleration is a dramatic pivot into optical.

The Optical Ramp: Credo’s Second Act

Here is what management committed to on the Q4 earnings call:

$600M+ in optical revenue in FY2027, with three distinct product lines each contributing more than $100M:

ZeroFlap Optical Transceivers — Credo’s existing optical solution offering 1,000x better reliability than traditional laser-based optics, with 2x lower power consumption

Optical DSPs (Robin & Cardinal) — Digital signal processors for optical channels, with accelerating design wins

Silicon Photonics PICs — From the DustPhotonics acquisition, enabling full vertical integration at 800G, 1.6T, and 3.2T speeds

The cadence is deliberate: mid-single-digit sequential growth in the first half of FY2027, followed by a significantly stronger second-half ramp as the optical portfolio hits scale.

The DustPhotonics Acquisition: A Strategic Masterstroke

On May 28, 2026 — one week before earnings — Credo completed the acquisition of DustPhotonics for $750M in cash plus ~0.92 million shares. DustPhotonics is an Israeli company developing industry-leading Silicon Photonics PIC technology for optical transceivers & adding silicon photonics PIC technology and covering 800G, 1.6T, and 3.2T optical connectivity — so they now own the full stack: copper cables, DSPs, and silicon photonics.

What does this mean in practical terms?

Before DustPhotonics, Credo designed the DSP (the brain of an optical transceiver) but sourced the silicon photonics chip (the physical component that converts electricity to light) from third parties. DustPhotonics gives Credo that chip in-house. The result is complete vertical integration across the optical connectivity stack:

SerDes IP → Digital Signal Processor → Silicon Photonics PIC → System Integration

This is the same vertical integration playbook Broadcom and Marvell have used to build moats over decades — except Credo is doing it at warp speed in the most important segment of the AI infrastructure buildout.

The $750M price tag is significant — it reduces cash from $1.3B to approximately $550M post-close. But at $140M+ quarterly FCF generation, Credo replenishes that within two to three quarters. And the return on that investment, if the $600M+ optical revenue target for FY2027 is achieved, is genuinely compelling.

The Moat: Narrow and Rapidly Widening

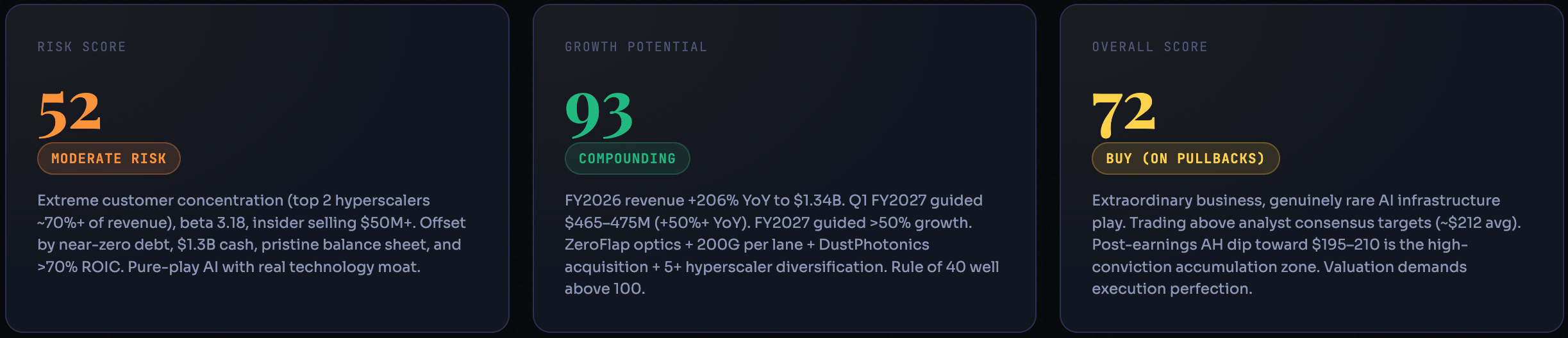

After more than three decades of semiconductor analysis, I have a healthy skepticism about “moat” claims. Too many companies claim moats that evaporate at the first competitive challenge. Credo’s moat is real, and here is the evidence:

68.1% gross margins. Hardware companies with no pricing power do not sustain 68% gross margins. The premium Credo commands prove the IP advantage is real and that hyperscalers value the reliability differentiation enough to pay for it.

70%+ ROIC. For every dollar invested in the business, Credo generates 70 cents in returns. This is a software company metric coming from a semiconductor designer. It reflects the IP-driven, asset-light nature of the fabless model — design is everything, manufacturing scale comes from TSMC.

The N-1 Node Strategy. While every other AI semiconductor company is fighting for TSMC’s most advanced nodes (the same queue as Apple and NVIDIA), Credo deliberately designs on mature, proven nodes one generation back. This delivers lower wafer costs, better supply certainty, and frees Credo from the bottlenecks plaguing cutting-edge node customers. It is a supply chain moat hiding in plain sight.

Hyperscaler Integration Depth. Getting qualified for use inside Amazon’s AI clusters is not a week-long process. It takes quarters of engineering collaboration, reliability testing, and system-level integration work. Once qualified, the switching cost is enormous — hyperscalers do not swap out embedded connectivity chips mid-cluster. Credo is embedded in the infrastructure of at least five hyperscalers, with at least three each generating more than 10% of revenue.

The Purple Cable Brand. In AI data center circles, Credo’s purple AEC cable has achieved something rare in B2B semiconductors: brand recognition. That AWS CEO photo was not an accident. It was a signal of how deeply embedded Credo is in the world’s most important AI infrastructure buildout.

The Competitive Landscape

Credo is not without competition. Understanding who they compete with and where Credo wins is essential.

Broadcom (AVGO, ~$840B market cap): Broadcom competes across the full networking stack — optical transceivers, custom ASICs, networking chips. For AECs specifically, Credo’s dedicated focus and purpose-built technology for short-reach copper creates a speed and reliability advantage that Broadcom’s more generalist approach has not matched at hyperscale.

Marvell Technology (MRVL, ~$215B market cap): Marvell’s PAM4 DSPs and custom silicon solutions compete in the broader AI connectivity space. Their optical DSP products could pressure Credo’s optical segment, but Marvell’s diversified focus means AEC is not a priority product line for them.

Astera Labs (ALAB, ~$47B market cap): The most direct peer in market cap terms. Astera focuses on PCIe retimers and CXL connectivity — a different layer of the AI stack. The two companies largely serve complementary roles inside the same clusters.

The honest assessment: Credo has a 2+ year lead in AEC deployment at hyperscale, and the DustPhotonics acquisition is pulling them ahead in optical as well. The moat is building, not eroding.

Valuation: Fairly Valued at $210, Attractive at $150

Let me be direct: CRDO is not cheap on traditional metrics. It never has been, and it should not be for a company growing at these rates.

The most reliable valuation method for hyper-growth semiconductors is the PEG method. With FY2027 non-GAAP EPS estimated at $6.00–7.00 on 80%+ growth, a PEG of 0.8–1.0 implies a fair value of $240–350. At post-earnings prices of $200–215, CRDO is at or below the low end of fair value on a PEG basis.

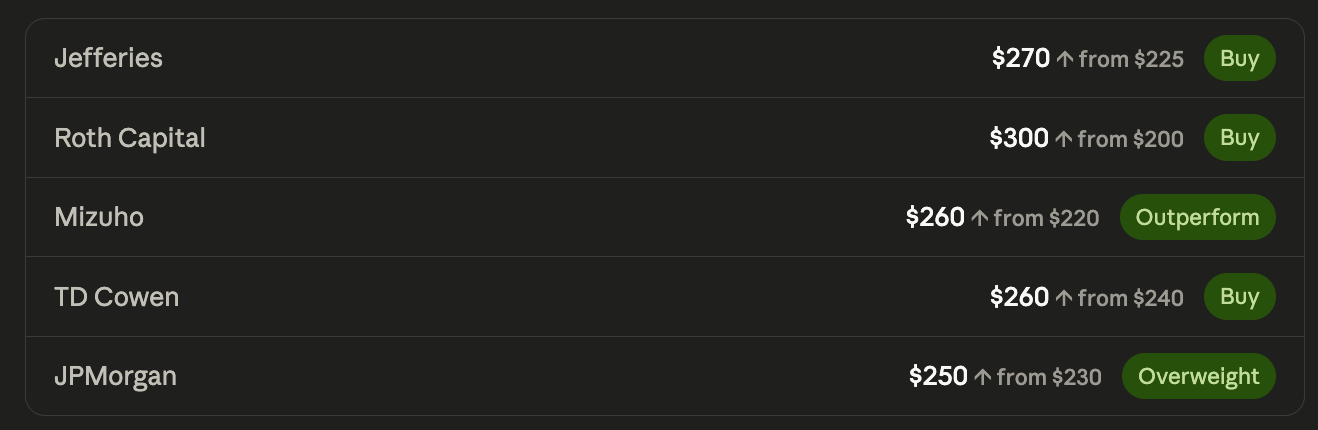

Post-earnings analyst price target raises confirm this view:

New consensus average: ~$250.91 across 18 analysts. Strong Buy is the dominant rating — 4 Strong Buy, 12 Buy, 1 Hold, 0 Sells.

The asymmetry at current prices: downside scenario (growth stalls, 10x FY27 P/S) implies ~$110–130. Upside scenario (80%+ growth delivers, multiple holds at 20x FY27 P/S) implies ~$340+. Risk/reward of approximately 2.5:1 favors the upside.

The Six Catalysts to Watch

Q1 FY2027 Earnings (August/September 2026): The first real test of whether the post-earnings dip was a buying opportunity or a warning. Watch for: Q2 FY2027 guidance above $490M, gross margin at 68%+, and DustPhotonics integration update. A guidance raise of this magnitude triggers a 15–20% re-rating.

DustPhotonics Optical Revenue Ramp (Q1–Q2 FY2027) Management committed to $600M+ in combined optical revenue for FY2027. Each quarter’s optical revenue disclosure will serve as a progress report on the $750M acquisition thesis. First hyperscaler design wins for the silicon photonics portfolio would be a material catalyst.

Customer Diversification (Ongoing FY2027) The single most important de-risking event for the stock’s multiple. A 5th or 6th hyperscaler crossing the 10% revenue threshold removes the concentration discount from the multiple. Watch quarterly filings closely.

200G Per Lane AEC Ramp (FY2027–FY2028) Credo leads today in 100G per lane AECs. The next generation is 200G. First volume orders from hyperscalers for 200G products confirm Credo maintains its generational lead and extends the product cycle through 2028 and beyond.

Active LED Cable (ALC) Sampling (FY2027) The next product innovation: AECs that reach up to 30 meters using LEDs instead of lasers. This opens a new adjacent market for row-scale and rack-to-rack connections. Management is committed to customer samples in FY2027, with initial revenue in FY2028. Design win announcements here unlock a $2B+ TAM expansion.

Analyst Price Target Convergence With the new consensus target at $250.91 and the stock near $212 post-dip, there is an 18%+ implied return just from mean-reversion to consensus. Continued target raises as analysts model in the $600M optical guidance and DustPhotonics synergies would provide a near-term re-rating catalyst.

The Risks — And I Will Not Sugarcoat Them

No investment of this quality exists without meaningful risks. I have watched too many high-growth stories end badly because investors ignored concentration risk.

Here is the unvarnished truth about CRDO: